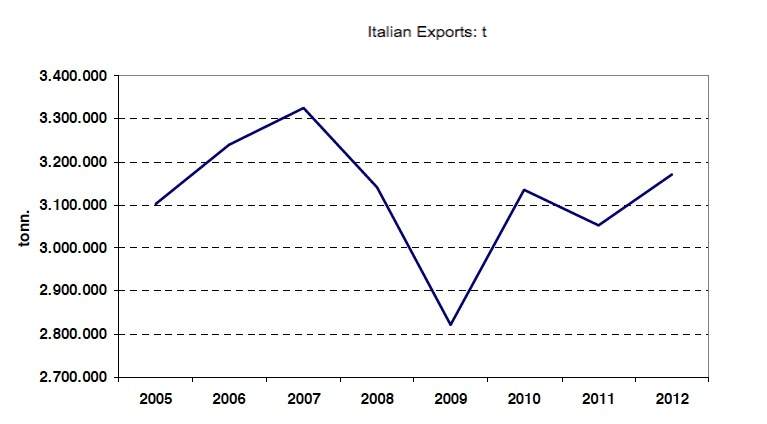

(May 2013) Italy’s natural stone branch shows sustained strength in exports as was calculated for 2012 by the Carrara-based Internazionale Marmi e Macchine (IMM): an increase by a strong 9.8% by value and 4.17% by tonnage as compared to 2011.

High-end, value-added products were also up: a positive development.

But the up-side holds true for only one part of Italy’s stone branch: closer examination is needed to determine whether exports truly made up for recessive demand according to a press release.

All in all Italy exported natural stone valued at a total of 1,810,421,274 € (~ 2,362 billion US-$). This equaled 4,178.259 t by weight coming again close to the pre-financial-level. The basis of the analysis are figures of the Italian Bureau of Statistics Istat.

Among the palate of stone varieties, marble was the front runner: broken down to value-added products exports were up +17% and reached 815,221,000 € or 885.119 t (+6%). The average price per ton was 921 € in this category, up by +11.2%

Spread across all types of stone included in the statistics the average value/ton was 221 € (previous year: 224 €).

Granite was also up (+3.2% to 549 million €) but receded in tonnage (-2.35% or 599,000 t).

As was the case before the financial crisis, commercial relations with North America were healthy and growing: Exports to USA and Canada reached levels of 337.5 million € (+27%) or 225,193 t (+14.6%). Note the high level of added value some 1,500 € (+11%).

Sales to Russia were comparatively low reaching a mere 40 million € (+9%) or 17,000 t (14.2%). But the average value/ton was an impressive 2,300 €!

As to Saudi-Arabia, a higher level than the 651 €/t attained could have been expected. Here Italy’s sales force seems not to have reached out to the wealthy clientele yet. Nevertheless exports reached 112 million € or +61%!

Relations to North Africa, where, at last count, uncertainty due to the civil turmoil surrounding the „Arab Spring“ had caused a recession in Italian exports, now also gave way to optimism. South of the Sahara, Angola, Kenya, and The Democratic Republic of Congo were the best customers.

Exports to other European countries, on the other hand, were weak by comparison (-1.6% to 472 million € or -4.4% to 639,000t). In absolute terms this was still more than the exports to North America. Strongest buyer was Germany with (+2.6% to 168 million € or -1.76% to 243,000 t). Exports to France reached 78 million € (+10.6) or 102,000 t (+6%).

Whereas the positive trend in exports of the last few years could be sustained, imports suffered a sustained setback: Marble and granite-imports were down from 393,964,783 € (-6%) or 1,490,333 t (-15%).

The main provider was India, albeit with a strong recession (value: -18.6%, tonnage: -25.4%). More material was purchased from Mozambique, Tunisia, and Albania.

The IMM Carrara expounds the positive balance of the natural stone branch valuing 1.4 billion €.

Tables: IMM Carrara

See also: